The Business of Autism Care: Financial Dynamics and Industry Trends

Before any honest analysis of applied behavior analysis cost in 2026, two events from April 2025 need to sit on the same page. In April 2025, the CDC's ADDM Network released its 2022 surveillance data and put US autism prevalence at 1 in 31 children identified by age 8 — up from 1 in 36 in the prior cycle. The same month, Roper Technologies acquired CentralReach for $1.85 billion — the largest behavioural-health software deal of the year and a quiet signal that the strategic value of an ABA practice-management platform is now north of where most analysts had it twenty-four months earlier. The two events are not unrelated. They sit on opposite ends of the same supply-and-demand curve.

This piece is an operator's map of that curve, in numbers. It is for the clinic founder weighing whether to expand to a second site, the BCBA-owner deciding whether to take a strategic investor's call, the PE associate building a thesis on an autism-care platform, the payer-side analyst staring at the 2026 CPT rate update, and the parent who searched for what ABA therapy actually costs and ended up here because every other page hand-waved the answer. It is anchored to applied behavior analysis cost (the 880-per-month query the consumer-facing pages handle badly), to ABA therapy business (the 40-per-month, $28.50-CPC operator query the trade publications gate-keep), and to the labor-economics question that is, on the available evidence, doing more to determine the industry's near-term trajectory than any other single variable.

A note before going further. This is industry analysis, not legal, financial, or operating advice. State-specific Medicaid rules and CPT billing decisions belong with a healthcare-billing attorney and a payer-relations specialist; investment decisions belong with a registered investment advisor; clinic-formation decisions belong with a state-licensed corporate attorney and a CPA. Where I cite numbers, the source is linked; where the right answer for your operation depends on judgement I am not in a position to make, I have said so explicitly.

The market, in figures

The US autism-care market does not have a single agreed top-line number, but the convergent estimates are close enough to be useful. Mordor Intelligence puts the global Applied Behavior Analysis market at USD 8.33 billion in 2026, projected to reach USD 10.39 billion by 2031 — a CAGR of 4.51 per cent, with the 2025 figure at USD 7.97 billion. North America accounts for roughly 61.74 per cent of the global total, which puts the US ABA market alone in the rough neighbourhood of USD 5 billion in 2026.

A few segment splits worth carrying:

- Pediatric vs adult. Children represent 86.02 per cent of the patient base. The adult segment is small (13.98 per cent) and growing fastest at 11.76 per cent CAGR — a structural shift driven by the cohort that aged out of childhood services in the late 2010s and early 2020s.

- Indication. ASD accounts for 70.10 per cent of ABA applications, with the remainder spread across developmental delay, behavioural concerns, and adjacent diagnoses.

- Setting. Center-based delivery is 55.02 per cent of the provider base. Home-based is the fastest-growing segment at 13.38 per cent CAGR, and telehealth supervision is growing at 13.84 per cent CAGR — both faster than the overall market.

The CDC prevalence figure is the demand-side counterpart. The April 2025 ADDM release reports 1 in 31 US children (3.2 per cent) identified with autism by age 8, with boys at roughly 1 in 20 and California at 1 in 12.5. Median age of diagnosis is 47 months. The implication for clinic operators is straightforward: addressable pediatric volume is rising, geographically uneven, and meaningfully concentrated in states with strong screening infrastructure.

What ABA actually costs in 2026

The single highest-volume search query in this cluster is applied behavior analysis cost. Most of the answers a parent finds on the first page of Google are vague. The honest version is straightforward and worth setting out before anything else.

National-average ABA hourly rates, as compiled by Autism Parenting Magazine, run roughly:

- Behavior Technician (BT) / Registered Behavior Technician (RBT): $50–$75 per hour

- Board Certified Behavior Analyst (BCBA): $100–$150 per hour

- Blended national average: approximately $120 per hour

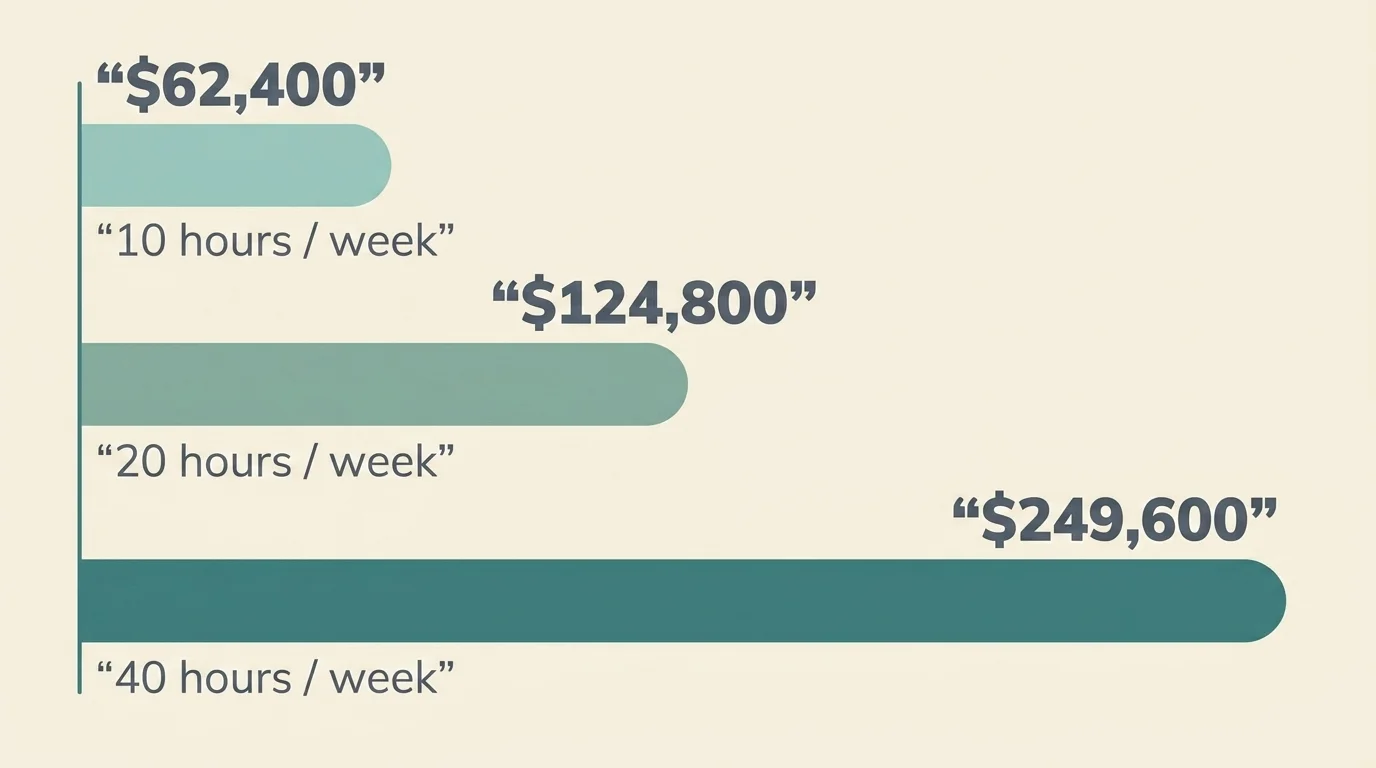

A typical recommended dose ranges from 10 to 40 hours per week, depending on the child's age, severity, and the clinical recommendation. The annual cost waterfall, at the $120 average and assuming private pay with no insurance offset:

- 10 hours/week: $62,400 per year

- 20 hours/week: $124,800 per year

- 40 hours/week: $249,600 per year

These are gross numbers. State autism mandates and commercial insurance materially reduce out-of-pocket costs in most states, often to a per-session co-pay between $20 and $50, but mandates vary. New York's mandate, for example, caps annual ABA benefits at approximately $45,000. The CDC has reported that families with an autistic child face roughly $17,000 to $21,000 per year in additional care-related costs compared with families of neurotypical children — a figure that captures the after-insurance reality more faithfully than the gross-rate numbers, even if it understates households that are paying for substantial private hours.

The boring version of cost advice for a family: get the diagnosis documented, file the insurance claim, find out what your state's mandate covers, then talk to a clinic about a billable plan and a separate cash-pay plan if hours are recommended above what insurance will fund.

The BCBA bottleneck

If you operate an ABA clinic in 2026, your single biggest operational variable is not your billing rate. It is whether you can hire and keep BCBAs. Salary negotiation in this market is one of the few places where the research and the folk wisdom roughly agree, and even then, the folk wisdom gets the reasoning wrong.

The numbers, restated plainly. The Behavior Analyst Certification Board's Lightcast 2026 report puts the active US BCBA workforce at approximately 75,600 in 2025. Job postings hit 132,307 the same year, up 28 per cent year-over-year. The same source reports that more than half of all US counties have zero practicing BCBAs and estimates the workforce gap at roughly five times the current supply. Job postings exceeded the active workforce by a factor of 1.75 in 2025 alone, which is the kind of ratio that does not happen in normal labour markets and that determines almost every other operating variable in this industry.

BCBA wage data from MyABAJobs (March 2025) puts median annual compensation at $73,616, with a working range of $74,000 to $90,500 and metro markets like Boston, Honolulu, and Newark above $100,000. State-level demand growth shows South Carolina up 102 per cent year-over-year, Utah up 94 per cent, Nebraska up 81 per cent — all states where wage trajectories should be set by the demand curve, not by the historical baseline.

The downstream pressure shows up in turnover. Industry surveys put behavioural-health worker burnout at 93 per cent reporting some level and 62 per cent at moderate-to-severe. Large agencies report annual turnover rates above 100 per cent — a number that means the average employee leaves before completing a year. Smaller centers report 77–89 per cent. RBT median turnover is roughly 65 per cent (above 90 per cent at some organisations), with average tenure around one year and 57 per cent of departing RBTs citing inadequate pay.

The boring version of staffing strategy in this market: every clinic's medium-term P&L is dominated by BCBA acquisition cost, BCBA retention, and the leverage ratio between BCBAs and BTs/RBTs you can sustainably operate. A growth strategy that does not solve those three things is, in this labour market, a deferred contraction strategy.

Reimbursement: where the margin lives

ABA reimbursement runs through a small set of CPT codes — 97151 (assessment), 97153 (direct treatment by a technician under BCBA supervision), 97155 (BCBA-delivered protocol modification), and 97156 (parent guidance) — with rates set independently by each state Medicaid program and by each commercial payer. The variance is bigger than most operating models reflect.

Two reference points from late 2025:

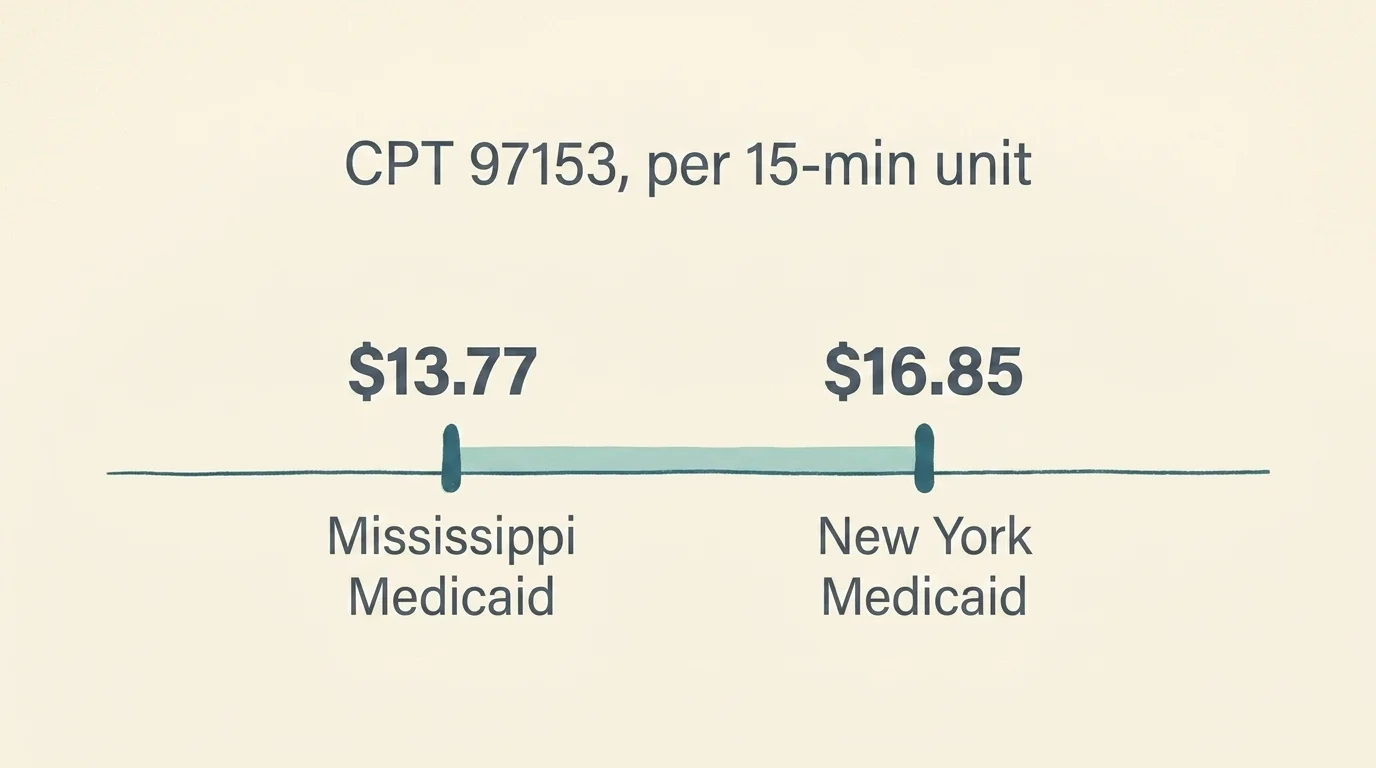

- New York Medicaid set CPT 97153 at $16.85 per 15-minute unit effective 1 October 2025, with a further reduction scheduled for April 2026.

- Mississippi Medicaid pays approximately $13.77 per unit of CPT 97153, per ProviderSpark's compilation.

That is roughly an 18 per cent rate spread on the highest-volume code in the ABA mix between two states neither of which is an outlier. State coverage of CPT 97155 (the BCBA-delivered code) has also been volatile through 2025: New Hampshire proposed dropping it in July before retracting in August; Virginia changed bundling rules in October in ways that materially affected providers' billing practices for months afterwards.

The implication for operating models: if a multi-state platform is treating CPT 97153 as a stable, fungible revenue line, the model is wrong. State-level rate dispersion plus mid-year policy shifts plus payer-mix variance combine to make payer-relations and billing infrastructure substantially more load-bearing than they look on a margin schedule. Verify rates with your state's Medicaid office before contracting, and assume mid-year rate or coverage changes will happen.

The 2026 PE roll-up: named deals and what they signal

ABA has been a private-equity roll-up category for roughly seven years. The pace did not slow in 2025; if anything, it accelerated. Mertz Taggart's Q1 2025 Behavioral Health M&A report documented behavioral-health dealmaking up 35 per cent year-over-year, with 12 transactions in the I/DD and autism segment in Q1 alone — the most for any quarter since 2021.

A short list of named deals from the last eighteen months, useful as a strategic reference rather than a complete map:

- Roper Technologies / CentralReach (April 2025). $1.85 billion. The strategic acquisition of the largest ABA EMR/practice-management platform by a software-focused holding company. Restated the strategic valuation of ABA back-office infrastructure.

- Goldman Sachs Alternatives / Center for Social Dynamics (late 2024). Direct-to-PE platform investment in a multi-state center-based ABA provider.

- Triton Pacific (via Already Autism Health) → Commonwealth ABA (January 2025). Platform-to-platform consolidation play.

- Nautic Partners / Proud Moments ABA (February 2025), from Audax. PE-to-PE secondary transaction; signal of holding-period rotation.

- Webster Equity Partners exited InBloom Autism Services (January 2026). Exit transaction reported by Behavioral Health Business.

The strategic pattern, restated: PE entry into ABA was thesis-driven on demographic demand (the rising prevalence curve) and operational arbitrage (consolidating fragmented markets). The 2025-2026 pattern is consolidation maturing into rotation — secondary transactions, exits to strategic buyers, and the layering-in of software platforms as separate strategic assets. The thesis that buying autism-care providers and growing them through site rollouts will reliably produce returns on a five-year hold is now, in an industry being asked to demonstrate outcomes, less defensible than it was when the first wave of buyouts cleared.

This is industry analysis. It is not investment advice. The specific question of whether a particular platform is correctly priced today belongs with an investment advisor and a diligence team, not with this article.

Clinic-model economics, briefly

The Mordor segment splits restated as operating decisions: center-based delivery (55 per cent of providers, mature growth), home-based (13.38 per cent CAGR), telehealth supervision (13.84 per cent CAGR).

The trade-offs operators actually navigate:

- Center-based. Highest BCBA leverage (one BCBA can supervise multiple BTs in adjacent rooms), highest fixed cost (real estate, build-out for sensory-appropriate spaces), highest utilization risk (empty rooms are pure cost).

- In-home. Lowest fixed cost, lowest utilization risk, but BCBA leverage is poor (drive time eats supervisory hours) and family-side scheduling friction is real.

- Hybrid. What most successful multi-site operators converge on. Center-based for the high-leverage hours; in-home for the families who cannot reliably get to a center.

- Telehealth supervision. The fastest-growing modality and the most contested. Some payers reimburse it at parity with in-person supervision; some at reduced rates; some not at all. Reimbursement risk is the binding constraint here, not clinical utility.

The operating playbook that consistently survives in this market combines center-based for leverage, in-home for reach, and telehealth supervision wherever payers will pay for it.

The 2026 outcomes reckoning

The strategic story I am most interested in for the next eighteen months is the one Behavioral Health Business named in November 2025 — payers and investors are increasingly pushing for proof-of-outcomes, and the consolidation-driven thesis of the 2018-2024 PE era ("buy and grow") is shifting toward an outcomes-driven thesis ("show the data"). The next round of payer contracts, in several states, is being written with measurable outcome requirements — adaptive functioning gains, parent-reported quality of life, school placement durability — rather than hour-volume metrics alone.

Two implications. First, the ABA platforms with credible outcomes infrastructure (standardised assessments at intake, mid-treatment, and discharge; integrated EMR-to-outcomes reporting; published external comparisons) will be advantaged in payer contracting and in strategic transactions. The CentralReach acquisition is, in part, a bet that the EMR platform that is best-positioned for outcomes reporting captures disproportionate strategic value. Second, the operators that are still optimising for billable hours alone will face a tightening payer environment over the next two-to-four years.

Tech investment is following this thesis. Motivity raised $27 million in March 2025 for an AI-driven ABA platform; the Autism Impact Fund invested in Unison Therapy Services the same month. These are early signals; the operating value of AI-driven outcomes prediction in clinical ABA practice is, today, mostly hypothetical. The strategic value of being seen to invest in it is, in payer-relations terms, much less hypothetical.

A short word on adjacent business questions

Two queries this article will get search traffic on, briefly:

- Autism franchise. A small number of established franchisors operate in this space (e.g., 360 Behavioral Health, Behavioral Innovations, Autism Learning Partners' affiliated programs), with franchise fees and royalty structures that vary significantly. The franchise model in ABA is more constrained than in restaurant or fitness categories because the regulated profession (BCBA supervision) cannot itself be franchised in the conventional sense. The franchise question is largely a real-estate-and-systems question with the clinical operation managed separately.

- Insurance and ABA business credit. This article does not cover the operating-finance side — line-of-credit structures, payer-receivable factoring, the impact of slow Medicaid reimbursement on working capital. Those questions belong with a CPA or controller experienced in behavioural health.

The short version

The US autism-care industry is roughly $5 billion in 2026, growing at low-single-digit rates structurally and faster in adults and home-based delivery specifically. Demand is rising as CDC prevalence climbs to 1 in 31. Supply is constrained by a BCBA workforce that is, by the certification authority's own data, several times smaller than the demand curve requires. The operating margin in any given clinic is dominated by BCBA acquisition, retention, and leverage. State Medicaid rates vary by 15-20 per cent on the highest-volume code and are policy-volatile in any given year. The 2018-2024 PE roll-up era is consolidating into a 2026-2028 outcomes-reporting era, and the platforms with credible data infrastructure will be advantaged in both payer contracting and strategic transactions.

This is what the data supports. The strategic decisions any specific operator, investor, or payer takes on the basis of it are, again, not advice this article can give — and any version of the conversation that does not eventually involve a healthcare-billing attorney, a payer-relations specialist, an RIA, or a CPA is a version of the conversation that has skipped the part where it gets real.

Frequently Asked Questions

Without insurance, ABA therapy at the national average of $120/hr runs roughly $62,400/yr at 10 hrs/wk, $124,800/yr at 20 hrs/wk, and $249,600/yr at 40 hrs/wk. State autism mandates and commercial insurance typically reduce out-of-pocket to a per-session co-pay of $20–$50, but mandates vary — New York's mandate caps annual ABA benefits at approximately $45,000. The CDC has reported that families with an autistic child face roughly $17,000–$21,000 per year in additional care-related costs.

Behavior Technicians (BTs) and Registered Behavior Technicians (RBTs) typically bill at $50–$75 per hour and deliver direct treatment under supervision. Board Certified Behavior Analysts (BCBAs) typically bill at $100–$150 per hour and provide assessment, protocol design, and supervision. The blended national average is roughly $120 per hour. The leverage ratio between BCBAs and BTs/RBTs is the single biggest driver of operating margin in a clinic.

Job postings for board-certified behavior analysts hit 132,307 in 2025 against an active workforce of approximately 75,600. The Behavior Analyst Certification Board's Lightcast 2026 report estimates the workforce gap at roughly five times the current supply. More than half of all US counties have zero practicing BCBAs. Annual turnover above 100% at large agencies (and 65% median RBT turnover) keeps the gap widening. The BCBA bottleneck is the binding constraint of the entire industry.

Reimbursement varies sharply by state. As of late 2025, New York Medicaid pays $16.85 per 15-minute unit of CPT 97153 (with a further reduction scheduled April 2026); Mississippi Medicaid pays $13.77 per unit. State coverage of CPT 97155 has also been volatile — New Hampshire proposed dropping it in July 2025 before retracting in August, and Virginia changed billing-bundling rules in October 2025. Verify current rates with your state's Medicaid office; assume mid-year rate or coverage changes will happen.

The market is fragmented but consolidating. Notable PE-backed players include Center for Social Dynamics (Goldman Sachs Alternatives), Proud Moments ABA (Nautic Partners, from Audax in February 2025), Commonwealth ABA (Triton Pacific via Already Autism Health, January 2025), and InBloom Autism Services (Webster Equity Partners exited in January 2026). The largest software/EMR platform CentralReach was acquired by Roper Technologies for $1.85 billion in April 2025.

The global Applied Behavior Analysis market is approximately $8.33 billion in 2026 and projected to reach $10.39 billion by 2031 (4.51% CAGR), per Mordor Intelligence. North America accounts for 61.74% of the global market. Children represent 86% of the patient base; the adult segment is smaller (14%) but growing fastest at 11.76% CAGR. Center-based delivery is 55% of the provider base; home-based is growing at 13.38% CAGR and telehealth supervision at 13.84% CAGR.

Behavioral Health Business reported in November 2025 that payers and investors are increasingly pushing for proof-of-outcomes in autism care. The next round of payer contracts in several states is being written with measurable outcome requirements (adaptive functioning gains, parent-reported quality of life, school placement durability) rather than hour-volume metrics alone. Platforms with credible outcomes infrastructure are being advantaged in payer contracting and strategic transactions; operators still optimising for billable hours alone face a tightening environment over the next two-to-four years.

A small number of established franchisors operate in ABA — fees and royalty structures vary significantly. The franchise model is more constrained than in restaurant or fitness categories because the regulated profession (BCBA supervision) cannot itself be franchised in the conventional sense; the franchise question is largely a real-estate-and-systems question with the clinical operation managed separately. The decision belongs with a state-licensed corporate attorney, a CPA experienced in behavioural health, and a payer-relations specialist.