Financial Planning for Families with Autistic Children: Strategies for Long-Term Stability

A grandparent I know — call him Bill — wanted to leave $40,000 to his autistic grandson when he died. He had never heard of an ABLE account. Bill was a careful man. He had spent his life building the kind of modest competence that produces $40,000 you can leave to one specific person at the end of it. He wrote his will so the money went, on his death, directly to his grandson's bank account. He thought he was doing the boring, sensible thing.

The boring sensible thing, in this case, was the wrong thing. Bill's grandson was on Supplemental Security Income (SSI) and the state Medicaid program, and the Social Security Administration's individual asset cap is $2,000 — a number that has not moved since 1989. The day the inheritance hit the bank, the grandson was suddenly $38,000 over the limit. SSI suspended his benefits the next month. Medicaid eligibility, which depends on SSI in most states, came up for review. The family spent the next four months unwinding what Bill had carefully wound. The money that was meant to make their son's life better made it, briefly, much harder.

I want to start there because every part of this article — ABLE accounts, special needs trusts, Medicaid waivers, letters of intent — is, in some form, an answer to that $2,000 cap. The instruments are not mysterious. The cost of not knowing about them is.

A note before going further. I am a writer, not a special-needs attorney or a Certified Financial Planner. The instruments below are accurate as of early 2026; the implementation details for your family — which trust type, when to fund it, how it interacts with your state's Medicaid program — are decisions you should make with a licensed special-needs attorney and a fee-only financial planner who specialises in disability families. The most expensive mistake in this niche is implementing a complicated instrument without one of those two people in the room.

What changed in 2026

The reason this article reads differently from what your search engine returned three years ago is that the federal landscape moved meaningfully in late 2025 and early 2026. Five updates worth knowing:

- ABLE Age Adjustment Act took effect 1 January 2026. Eligibility for an ABLE account, previously limited to people whose disability began before age 26, now extends to people whose disability began before age 46. The Arc estimates roughly 6 million additional Americans now qualify, bringing the total eligible population to about 14 million, including roughly 1 million veterans.

- 2026 ABLE annual contribution limit is $20,000, up from $19,000 in 2025. The cap moves with the federal annual gift-tax exclusion (Disability Scoop, December 2025).

- ABLE-to-Work is now permanent. Working ABLE account owners without an employer retirement plan can contribute up to $15,650 above the $20,000 cap — a potential annual total of $35,650.

- The Saver's Credit now applies to ABLE contributions. Eligible contributors can claim a tax credit of up to 50 per cent of the first $2,100 contributed, for a maximum credit of $1,050.

- 529-to-ABLE rollovers are now permanent. A previously time-limited rule allowing 529 college-savings funds to roll into an ABLE account (subject to the annual ABLE cap) was made permanent under the One Big Beautiful Bill Act.

The headline takeaway: more people are eligible, the ceilings are higher, and the tax incentives are stronger than they were two years ago. A family that wrote off ABLE in 2023 because their child's diagnosis came later may want to re-check.

The $2,000 problem

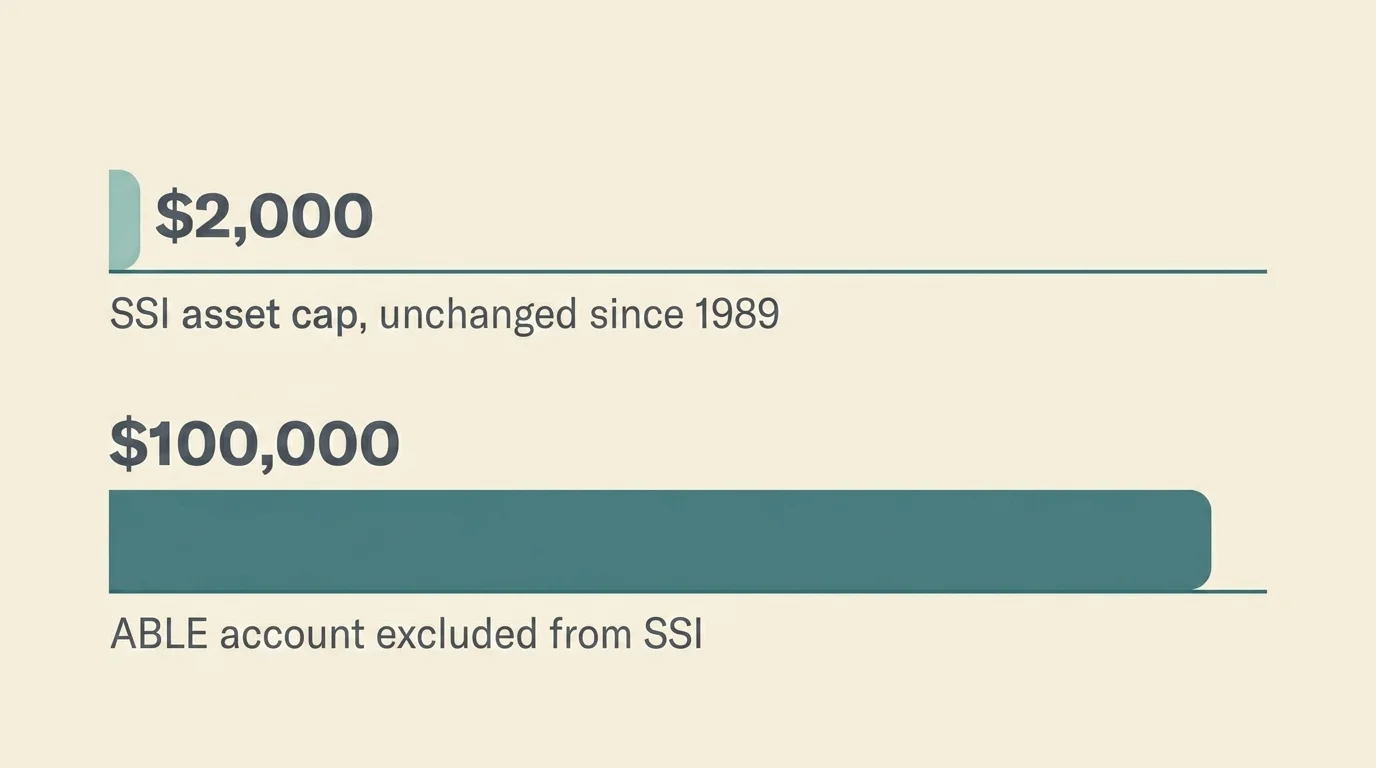

Most American autism families that depend on government benefits live with one fact in the background of every financial decision: SSI's individual asset cap is $2,000 (or $3,000 for a couple). This number has not been adjusted for inflation since 1989. It is, in real terms, roughly 53 per cent of what it was when it was set. It is also a hard cliff: cross it, and benefits suspend.

The boring version of this advice: any financial planning for a child receiving (or likely to receive) SSI must treat the $2,000 cap as the binding constraint, and every meaningful instrument in this article exists to get around it without losing eligibility. ABLE accounts and special needs trusts are not exotic estate-planning vehicles. They are the standard tools for keeping inherited or saved money from triggering the cap.

Two practical implications:

- Talk to grandparents and other potential gift-givers early. Bill did not know. The next Bill in your family does not know either. The conversation is uncomfortable and considerably less expensive than the unwinding.

- Do not put more than $2,000 into a child's bank account or directly in their name. The first $100,000 in a properly opened ABLE account is excluded from the SSI asset limit. Most other ways of holding money for a disabled child are not.

ABLE accounts: what they are and how to use one

An ABLE account is a tax-advantaged savings and investment account in the disabled person's name, structurally similar to a 529 college-savings account. The account holder owns and controls it (with a representative payee where appropriate). Earnings grow tax-free. Withdrawals for "qualified disability expenses" — a deliberately broad category covering housing, transportation, education, employment training, assistive technology, healthcare, financial management, and basic living expenses — are tax-free. The first $100,000 in the account does not count against SSI's $2,000 asset cap. (The Arc is the cleanest single primer.)

The 2026 contribution limits, restated in plain terms:

- $20,000 a year from any contributor (the account holder, parents, grandparents, friends, the child's own earnings) — capped at the federal annual gift-tax exclusion.

- Up to $15,650 more if the account holder works and has no employer retirement plan, under the now-permanent ABLE-to-Work provision. Total potential annual contribution: $35,650.

- Up to $1,050 in Saver's Credit for eligible contributors (50 per cent of the first $2,100 contributed).

- 529-to-ABLE rollovers are permanently allowed, subject to the annual ABLE cap.

ABLE programs are run state by state. Forty-seven states plus DC operate their own; the three that don't (North Dakota, South Dakota, Wisconsin) leave their residents to use another state's program. Most state programs accept non-residents. Fees, investment options, and minimum opening balances vary; the ABLE National Resource Center maintains the canonical comparison.

The boring version of opening one: for most families, the cost-benefit math says open the home state's program if it has one and it is competitive on fees, otherwise compare a couple of out-of-state options. Pick a low-cost age-appropriate investment option. Set up automatic monthly contributions if cash flow allows. Do not let the balance drift above $100,000 without a clear plan.

Special needs trusts: third-party, first-party, pooled

A special needs trust (SNT — also called a supplemental needs trust) is a legal arrangement in which a trustee holds and manages assets for the benefit of a disabled person without those assets counting as the beneficiary's own resources. There are three flavours, and confusing them is the second most expensive mistake in this niche after the $2,000 cap.

- Third-party SNT. Funded with someone else's money — typically a parent's or grandparent's. This is the SNT Bill should have used. Assets do not affect the beneficiary's SSI or Medicaid. On the beneficiary's death, remaining assets pass to whoever the grantor named.

- First-party SNT (sometimes "(d)(4)(A) trust"). Funded with the beneficiary's own money — usually a personal-injury settlement, an inheritance the disabled person was named as direct beneficiary on, or savings from earnings that pushed them over the SSI cap. Same asset-exclusion benefit, but with one important consequence: on the beneficiary's death, Medicaid is reimbursed first for the lifetime cost of services, before remaining assets pass to family. This is the so-called "Medicaid payback" rule.

- Pooled SNT. Run by a non-profit, pooling the funds of many beneficiaries for investment purposes while keeping individual sub-accounts. Typically lower drafting and administrative costs than a standalone trust, useful for smaller funded amounts where the cost of a standalone trust outweighs the benefit.

Specialneedsanswers.com's comparison page is the canonical mainstream summary; it is worth a parent's full read.

What it costs

Drafting a standalone third-party SNT typically runs $1,500 to $5,000 in attorney fees in the United States, with substantial state-by-state and complexity variation. Ongoing trustee fees often range 0.5 per cent to 1.5 per cent of assets per year, depending on whether you use a corporate trustee, a family member, or a non-profit. A pooled SNT is usually the lower-cost option for funded amounts under roughly $100,000–$150,000. A licensed special-needs attorney in your state is the right person to confirm the actual numbers.

The honest version of this advice: do not draft your own SNT from a template. The instrument depends on state law, the interaction with SSI and Medicaid is technical, and a trust that does not properly preserve eligibility is, financially, worse than no trust at all.

ABLE vs SNT: which one (and the case for both)

The decision parents most often want resolved on a search engine is which instrument to use. The honest answer, endorsed by the ABLE National Resource Center and most special-needs planners, is that for most autism families both instruments will eventually be needed and that they do different jobs.

A working comparison:

| Question | ABLE account | Special needs trust |

|---|---|---|

| Who owns/controls it | The disabled person (or representative payee) | A trustee, on behalf of the beneficiary |

| Annual contribution cap | $20,000 / $35,650 with ABLE-to-Work (2026) | None |

| Setup cost | Free or near-free | $1,500–$5,000 typical drafting |

| Annual cost | Low fees ($25–$100 typical, plus investment fees) | 0.5%–1.5% of assets, plus admin |

| Tax treatment | Earnings grow tax-free; qualified withdrawals tax-free | Trust income taxed; distributions to beneficiary may have tax effects |

| SSI asset effect | First $100,000 excluded | Properly drafted SNT does not count |

| Medicaid payback at death | None (state Medicaid recovery in some cases — varies) | First-party: yes; third-party: no |

| Best for | Routine spending; smaller balances; what the disabled person controls | Larger inheritances; lifetime asset management; what someone else controls |

| Eligibility (2026) | Disability onset before age 46 | Any disabled beneficiary |

The practical pattern most families end up with: an ABLE account for everyday spending and the cash that the disabled person needs to control, plus a third-party SNT for any inheritance or large gift. Cash sitting in the SNT can be funnelled to the ABLE account up to the annual cap; trust-to-ABLE transfers do not count as income to the beneficiary, while direct cash distributions from a trust still reduce SSI dollar-for-dollar. That mechanic alone is most of the case for having both.

Autism Parenting Magazine's piece on this question gives the autism-specific framing in clearer-than-usual language; it is worth bookmarking.

Medicaid HCBS waivers, briefly

Routine Medicaid covers acute medical care. The big practical question for many autism families is what covers the long-term, in-home, behavioural, and community-based services that are not acute medical care — the ABA hours that exceed insurance caps, the in-home behavioural support, respite care for the parents, community integration programs, day services for older children. The answer, in most states, is a Medicaid Home and Community-Based Services (HCBS) waiver.

Two facts every family should know about HCBS waivers:

- Coverage varies dramatically by state. Eligibility, the specific services covered, the age cap, and the income/asset thresholds for the disabled child (often calculated independently of the parents' income for waiver purposes) are all set state by state. The Arc's state directory is the most accessible starting point; your state's Medicaid office is the authoritative source.

- Waitlists are real and long. Most states have multi-year waitlists for autism waivers — often 3 to 7 years, sometimes longer. The single highest-leverage move many families miss is applying as soon as the diagnosis is in hand, regardless of whether services are immediately needed. The waitlist clock starts at application. Verify with your state's Medicaid office.

The waiver landscape is also where a great deal of money is. The HCBS waiver search has a $11.69 cost-per-click on Google because advertisers know the value of the services involved. The boring version of this advice is that the application is often more bureaucratic than complicated, and the cost of putting it off is substantial.

The letter of intent

A letter of intent is a non-binding document a parent writes to describe everything the next caregiver — successor trustee, family member, group home staff, case manager — will need to know in order to take over the daily life of the autistic person. It is not a legal instrument. It does not move money. Every successor caregiver will rely on it.

A working outline:

- The person. Their personality, communication style, what they like and dislike, what gives them comfort, what causes distress. The texture of who they are.

- Daily routines. Wake, meals, hygiene, school or day program, exercise, evening, sleep. The level of detail a stranger would need to keep the day functioning.

- Sensory profile. What they are hypersensitive to, what they seek, what calms them, what tools and accommodations work. Where their stims sit.

- Medical. Diagnoses, medications, allergies, physicians, dentists, therapists, hospital preference, advance directives where applicable. The numbers to call.

- Education or program. Current placement, IEP or service plan, key teachers and aides, accommodations that work, transitions that are difficult.

- Communication. How they communicate, what AAC they use, how they say yes and no, how they ask for help.

- Future hopes. What life you want for them, what you would not want, what work or community engagement would suit them, what living arrangements you have considered.

The letter is updated annually or when something significant changes. A copy goes to the trustee and to a designated family member. It is the document none of the financial instruments above can replace and the cheapest one in this article to write.

The $30K crisis playbook

When a Bill-style situation arises — an inheritance, a settlement, a grandparent gift, a sudden lump sum that will exceed the SSI $2,000 cap — there is a rough sequence that minimises damage:

- Contact a special-needs attorney the same week. Not next month. The clock starts the day the asset arrives.

- Move what fits into the ABLE account. Up to $20,000 of new contributions per year (plus ABLE-to-Work up to $35,650 if applicable). Note this does not move the source's character — funds going into ABLE from the disabled person's hands, having briefly belonged to them, count toward the annual cap.

- Establish or fund the appropriate SNT for the remainder. First-party if the money was in the disabled person's name (the inheritance arriving directly into their account); third-party if a relative is restructuring how they intended to give. The attorney makes this call, not the internet.

- Notify SSA and the state Medicaid office through the appropriate channels and timelines. Hiding the asset is not a strategy; properly characterising it is.

- Update the letter of intent to reflect the new financial structure for whoever comes next.

The unifying point: most $2,000-cap crises are recoverable if addressed within the same month and difficult to recover from if left to drift. Speed and the right professional are most of the work.

The boring version

For most American autism families: open an ABLE account in your home state's program (or a competitive out-of-state program if your state's is poor), draft a third-party SNT with a special-needs attorney once you have meaningful assets to leave or expect to receive, apply for your state's HCBS Medicaid waiver as soon as the diagnosis is in hand regardless of current need, and write a letter of intent and update it once a year.

This advice will not help you if you are at the very low end of the asset spectrum and primarily need help paying for therapy this month — that is a different conversation, mostly about waivers, sliding-scale programs, and your state's specific autism funding pathways. It will not help you if you are at the very high end where private trust planning, life insurance funding strategies, and tax-advantaged giving are dominating the math — that is a conversation for a fee-only financial planner specialising in disability families. For the median family in between, the four instruments above are roughly the toolkit.

Bill's family eventually reorganised. The grandson's benefits restored after four months. The $40,000 ended up in a properly drafted third-party SNT, with a portion funnelled into a newly opened ABLE account each year for everyday spending. The story has a defensible ending. It would have been a much shorter and much less expensive story if Bill had had this conversation with a special-needs attorney before he wrote his will.

Frequently Asked Questions

The single most important fact for autism families relying on government benefits is the SSI individual asset cap of $2,000 (unchanged since 1989). Every meaningful financial instrument in this niche — ABLE accounts, special needs trusts, Medicaid HCBS waivers — exists to hold money for a disabled person without crossing that cap and triggering benefit suspension. Routine costs include therapy out-of-pocket, specialised education, equipment, and respite care, all of which vary widely by state and by the child's specific support needs.

The practical budgeting question for most autism families is not where to cut spending but where to put money so SSI and Medicaid eligibility are preserved. An ABLE account holds up to $20,000 a year (plus up to $15,650 more under the now-permanent ABLE-to-Work provision) tax-free, with the first $100,000 excluded from the SSI asset cap. Withdrawals for qualified disability expenses — housing, transportation, education, employment training, healthcare, basic living — are tax-free. For larger assets and longer-horizon planning, a properly drafted special needs trust holds the money outside the beneficiary's name.

A special needs trust (also called a supplemental needs trust) is a legal arrangement in which a trustee holds and manages assets for a disabled beneficiary without those assets counting as the beneficiary's own resources for SSI or Medicaid purposes. Third-party SNTs are funded with someone else's money (usually a parent or grandparent); first-party SNTs are funded with the beneficiary's own money (a settlement, an inheritance) and are subject to Medicaid payback at death. Drafting typically costs $1,500–$5,000 with a special-needs attorney.

An ABLE account is a tax-advantaged savings and investment account the disabled person owns and controls, capped at $20,000 a year in 2026 ($35,650 with ABLE-to-Work). A special needs trust is a legal arrangement with a trustee managing assets for the beneficiary, with no annual contribution cap. Most autism families benefit from both — the ABLE account for everyday spending, the SNT for larger inheritances. Trust-to-ABLE transfers do not count as income to the beneficiary, while direct trust cash distributions reduce SSI dollar-for-dollar.

As of 1 January 2026, anyone whose disability began before age 46 (up from age 26 under the prior rule) qualifies. The ABLE Age Adjustment Act expanded eligibility to roughly 6 million additional Americans, including about 1 million veterans, bringing the total eligible population to approximately 14 million. Eligibility does not require the person to currently be under 46, only that the qualifying condition began before that age.

$20,000 per year from any contributor (the account holder, parents, grandparents, friends, the holder's own earnings), capped at the federal annual gift-tax exclusion. Working account holders without an employer retirement plan can contribute up to $15,650 more under ABLE-to-Work — a potential annual total of $35,650. Eligible contributors can also claim the Saver's Credit (up to 50% of the first $2,100 contributed, max $1,050). The first $100,000 in the account is excluded from the SSI asset limit.

State-run Home and Community-Based Services (HCBS) waivers can cover services routine Medicaid does not — in-home behavioural support, respite care for parents, community integration programs, day services, ABA hours that exceed insurance caps. Coverage, eligibility, and the income/asset thresholds vary dramatically by state. Most states have multi-year waitlists (often 3–7 years), so apply as soon as the diagnosis is in hand, regardless of immediate need. Verify with your state's Medicaid office.

Attorney drafting typically runs $1,500–$5,000 for a standalone third-party SNT, with substantial state-by-state and complexity variation. Ongoing trustee fees often range 0.5%–1.5% of assets per year, depending on whether you use a corporate trustee, a family member, or a non-profit. A pooled SNT — run by a non-profit pooling many beneficiaries' funds — is usually the lower-cost option for funded amounts under roughly $100,000–$150,000. A licensed special-needs attorney in your state is the right person to confirm the actual numbers.

A letter of intent is a non-binding document parents write to describe everything the next caregiver — successor trustee, family member, group home staff, case manager — will need to know to take over the daily life of the autistic person. It covers personality, daily routines, sensory profile, medical, education, communication style, and future hopes. It is not a legal instrument and does not move money, but every successor caregiver will rely on it. Update annually. Yes, write one.